Free tools & templates

These spreadsheet tools, designed by our team of accountants, auditors and CPAs, help you transition, close and calculate. These tools can get you started—for fully-featured solutions, see our software.

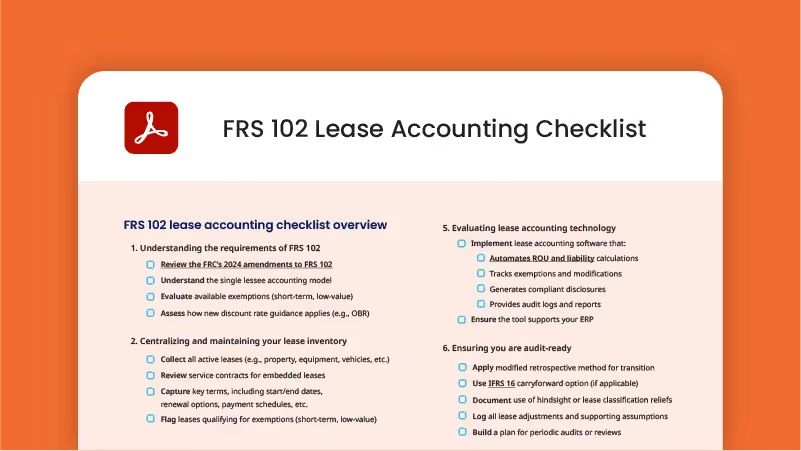

FRS 102 Lease Accounting Checklist

A step-by-step guide to prepare for, and maintain, compliance under the new UK GAAP lease accounting standard

.avif)

Summit On-demand: Building a Successful Tech Stack With NetSuite

Derek Hitchman examines strategies to integrate supporting technologies, ensuring they work together to streamline processes and drive innovation

Summit On-demand: Conquering Your Month-end Close

This session is designed to help finance professionals take control of the close with strategies for improving speed, accuracy, and team coordination

Summit On-demand: Toward the Sounds of Chaos

Lee Jacobs, SquareWorks Head of Product, leads this session on learning how to guide your team through complex AP challenges

Summit On-demand: Vibe Coding for Accountants

Learn how to automate accounting processes, share best practices for AI, and map out how you can start building customizations that save time.

Summit On-demand: Project Accounting, Job Costing & Grant Management

Learn how to streamline job costing, track grants with confidence, and maintain compliance with ASC 606—without sacrificing productivity.

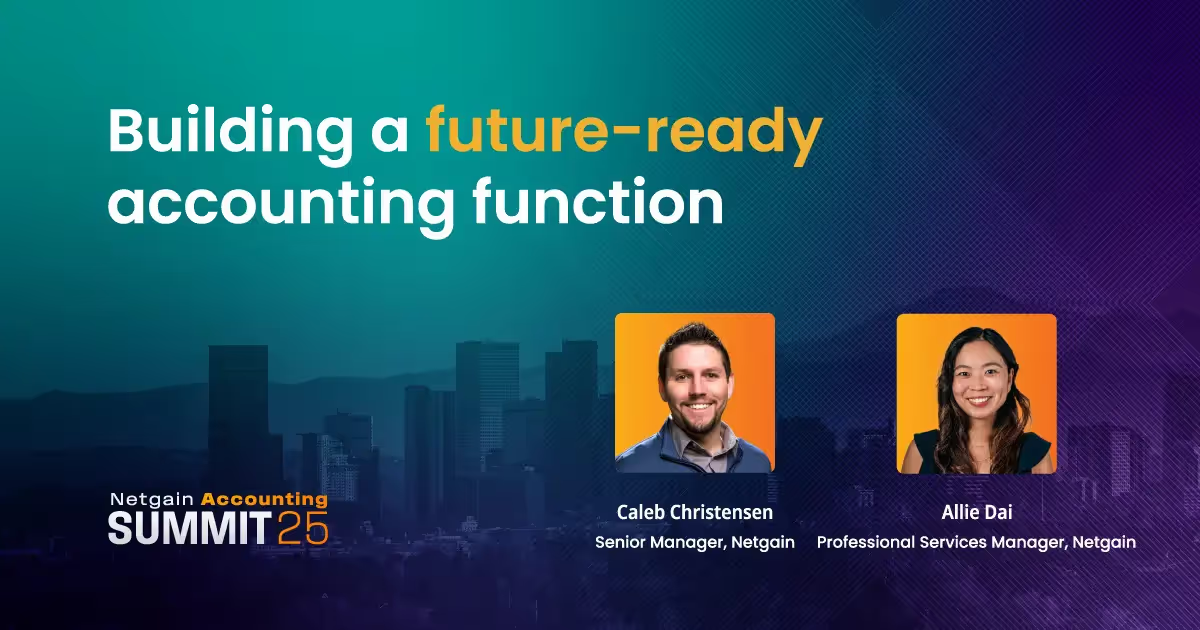

Summit On-demand: Building a Future-Ready Accounting Function

Learn how to identify your team’s current maturity level, plan the next steps for growth, & leverage modern systems to improve efficiency

Summit On-demand: How To Be a Great NetSuite Administrator

Learn strategies to empower end users to get the most out of NetSuite, ensuring higher productivity and a smoother user experience

Summit On-demand: AI in Action for Accounting Teams

This session explores native AI features available in NetSuite today and how businesses are extending them with custom-built tools to boost efficiency

.avif)

Summit On-demand: Closing Keynote

An inspiring session on embracing change and preparing for the future of accounting.

Summit on-demand: Opening Keynote

Adam Riches kicked off our first Netgain Accounting Summit with a 30-minute keynote

Bank reconciliation Excel template

Quickly match transactions and reconcile accounts with this Excel-based bank reconciliation template.

The Definitive Guide to Modernizing Your Month-End Close

The month-end close process can feel like a recurring nightmare. Inefficiencies, manual tasks, and errors make it a stress-inducing burden. But the right tools and mindset can transform a last-minute rush into a seamless operation that adds strategic value to your organization. This e-Book will guide you through five steps to transform your close process into a smarter, faster, more reliable operation.

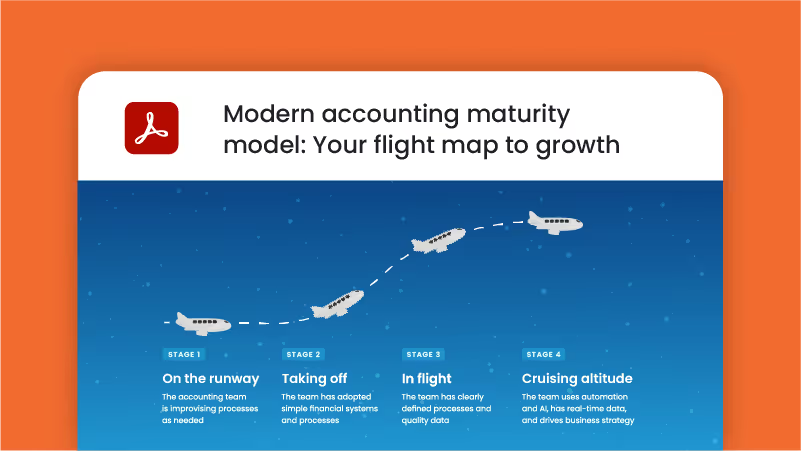

Modern accounting maturity model: Your flight map to growth

As your business grows, your accounting function must grow with it. But the industry is evolving rapidly, and growing your accounting department with modern systems can feel like uncharted territory. That’s why we put together this modern accounting maturity model to help you plan your flight path. Download the e-book to explore the path to maturity.

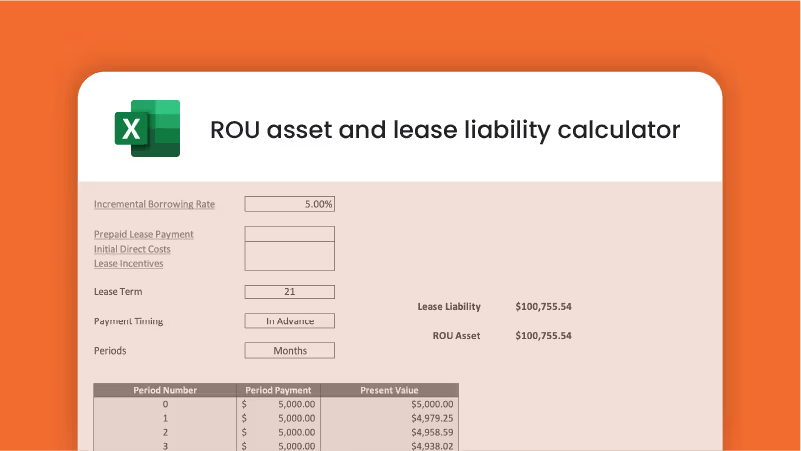

ROU asset & lease liability calculator

Calculate the net present value of lease payments, including prepayments, costs, and incentives with this ROU calculator.

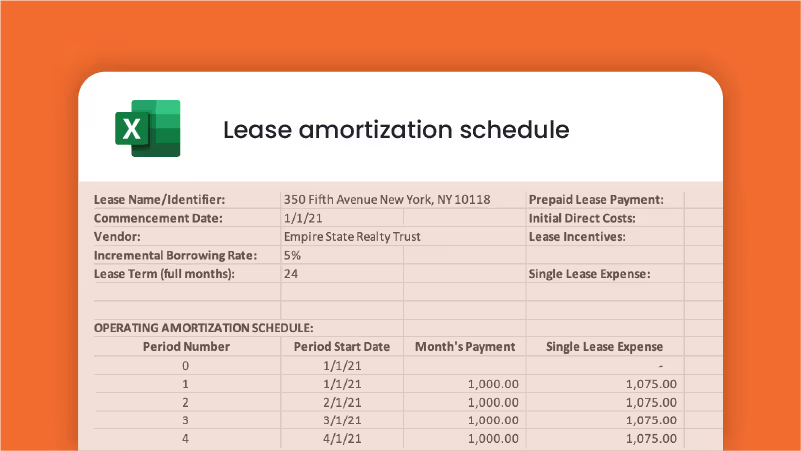

Lease Amortization Schedule Excel Template (ASC 842) | Netgain

Track lease payments and stay ASC 842 compliant with a step-by-step amortization schedule for accurate reporting.

Fixed asset accounting checklist

Stay compliant and in control with a detailed fixed asset accounting checklist that covers every step from acquisition to disposal.

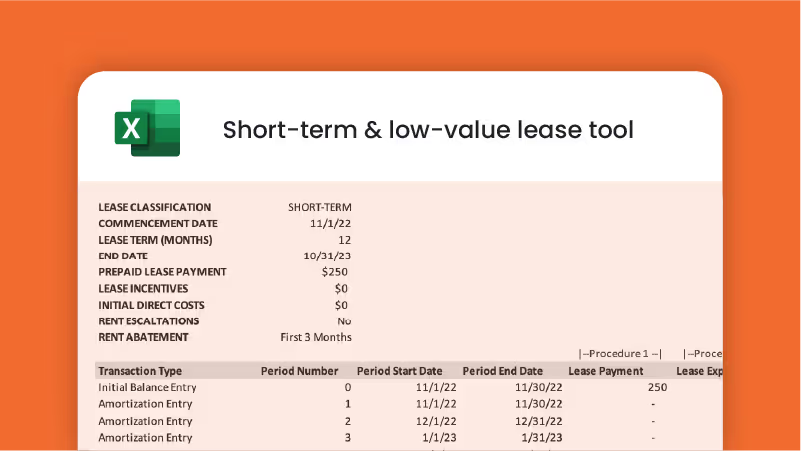

Short-term & low-value lease tool

This workbook will help you calculate the schedule for lease payment, lease expense and deferred rent using short-term and low-value lease exemptions.

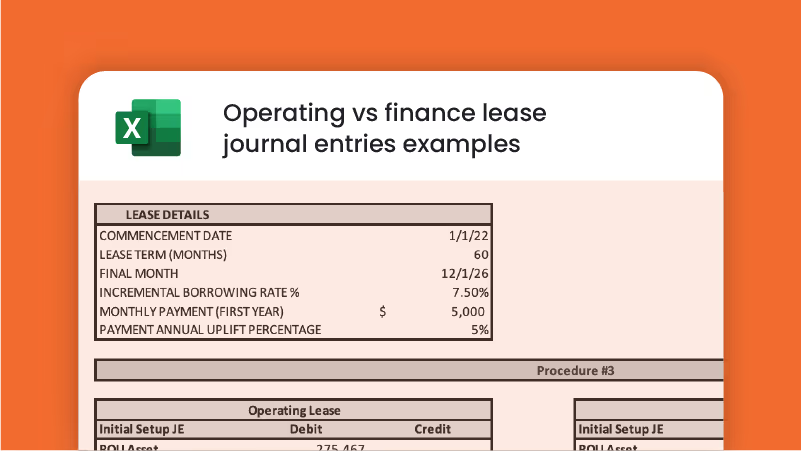

Operating vs finance lease journal entries examples

See typical ASC 842 journal entries for operating and finance leases and understand their financial statement impact.

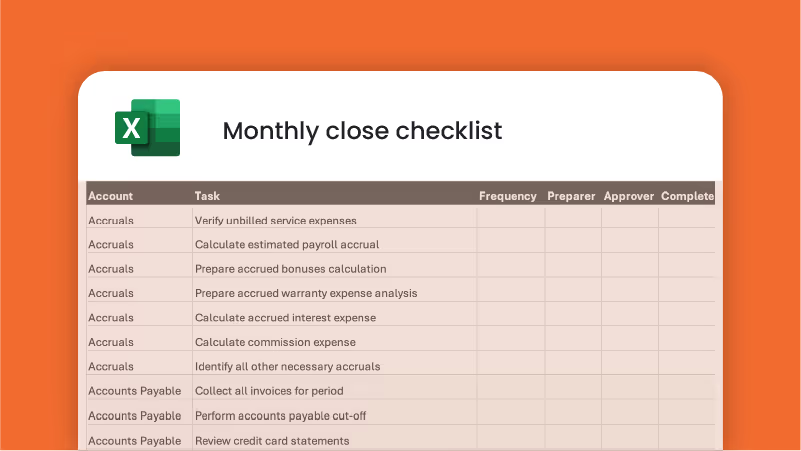

Month-end close checklist

Speed up your month-end close and reduce manual errors with a checklist built for consistent, accurate financial reporting.

Lease vs. loan calculator (seller's perspective)

Compare leases vs. loans under ASC 842 and see financial impacts from the lessor’s perspective using this interactive workbook.

Lease vs. buy calculator

Compare leasing vs. buying side by side and make data-driven decisions with tax and cost insights from this calculator.

Financing leases schedule and guide

Use this workbook to convert financing leases from ASC 840 to ASC 842 with auditor-style structure and compliant formatting.

Discount rate calculator

Identify the right risk-free rate and understand the formulas behind it with this calculation and insight tool.

Accounting policy memo example

Document the method used to calculate your discount rate as additional support for your auditors.

ASC 842 disclosure report example

See example disclosure calculations for operating and financing leases with this ASC 842 workbook.

ASC 842 guide for auditors

Equip your team to perform efficient ASC 842 audits with this guide designed to improve audit outcomes and client satisfaction.

Accounting software evaluation checklist

Assess your NetSuite setup and find new ways to boost ROI, efficiency, and automation with this step-by-step checklist.